In the coming years, the growth of ICT in China is expected to outperform on a regional and global basis.

China

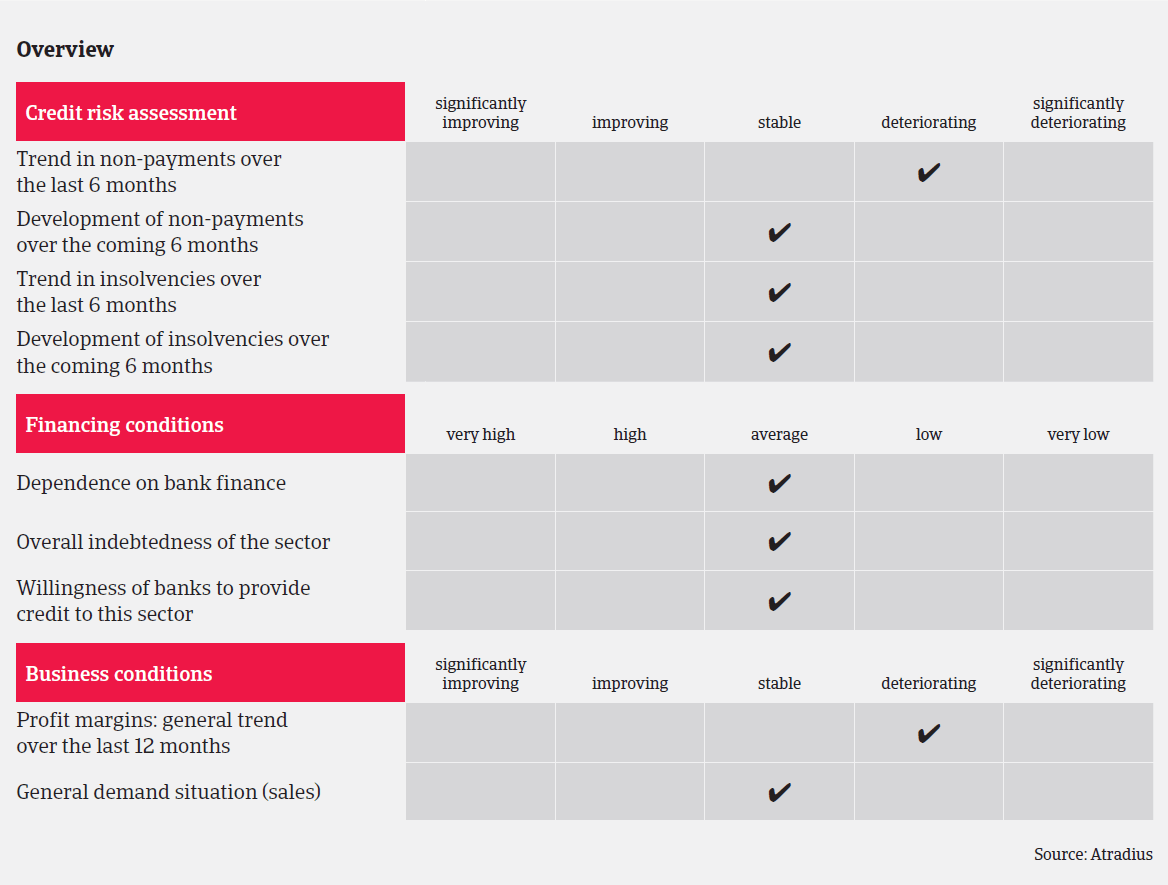

- High sales growth expected to continue

- Margins have deteriorated

- More payment delays over the past six months

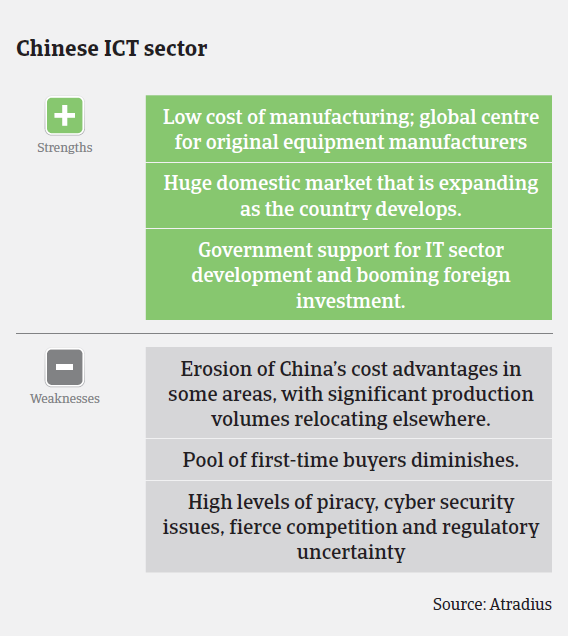

Given the low cost of manufacturing, China is the global centre for ICT original equipment manufacturers, with a large number of production bases of ICT multinationals as well as small- and medium-sized local manufacturers. In terms of wholesale and distribution, the majority of businesses are small-sized companies, also helped by the low market entry barriers. There are afew medium and large-sized ICT traders in China with channel coverage of certain regions or the whole country.

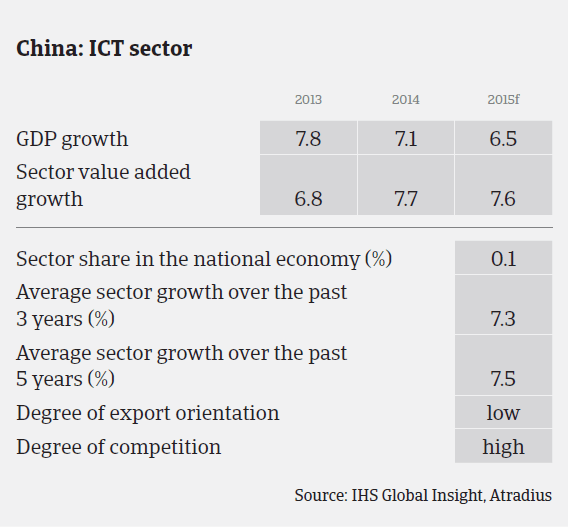

According to the research institute BMI, ICT spending in China reached CNY 870.9 billion (EUR 130.4 billion) in 2014, a year-on-year increase of 9.9%, after increasing 8.9% in 2013. The higher growth was triggered by the withdrawal of support for the XP operating system by Microsoft in April 2014 as well as a series of reforms announced by the Communist Party in late 2013 (e.g. urbanisation development and reform of the one-child policy). Wider support for the services sector and modernisation of state-owned enterprises, including finance, telecommunications, healthcare, education and professional services (e.g. call centres) will be the most important reforms for boosting the ICT sector further, with software and services well placed for faster growth.

There have also been changes in ICT market regulations, including easing restrictions on game console sales and allowing foreign investment in the mobile valued added service market,which bode well for further liberalisation in the medium term. One area of rapid development is the cloud computing market in China, with domestic and global vendors targeting the marketwith a range of services.

In the coming years, the growth of ICT in China is expected to outperform on a regional and global basis. The country’s large population, rising incomes and low device penetration boost ICT spending on the consumer’s side. A supportive policy environment and reforms through to 2020 will fuel ICT investment from the government and businesses. The rural and SME markets are expected to be the two highest growth segments for ICT, given that both are vast and still underpenetrated. BMI forecasts China’s ICT spending will increase 8.8% in 2015, to CNY 947.5 billion (EUR 141.8 billion).

That said, China’s ICT market is not without challenges as the pool of first-time buyers diminishes and vendors struggle with high levels of piracy, cyber security issues, fierce competition, price-sensitive consumers and eroding margins. As the market matures, vendors offering hybrids/convertibles and service businesses with strong cloud computing product portfolios are expected to outperform.

In 2015, China’s ICT market will remain hardware-centric. Computer hardware sales are expected to increase 6.3% in 2015 to CNY 596.9 billion (EUR 89.4 billion), boosted by rising incomes and the low device penetration rate. PC penetration in China’s rural areas is only 24%, far below that of 97% in first-tier cities. Vendors will continue tapping the growth potential of China’s rapidly expanding middle class and underpenetrated low income second-tier city and rural markets in 2015. The increasing availability of low-priced Android-based tablets will boost overall spending. Economic, political and social reforms through to 2020 should mark the beginning of a new wave of investment by state-owned organisations and the private sector.

However, foreign brands are facing downward pressure in China due to the new government’s preference for local brands, especially after Snowden’s revelations of US data monitoring. Additional risk of cyber security and data sovereignty concerns have led to increased protectionism between the US and China. An increasing number of US vendors has started to cooperate with Chinese companies to manufacture products under local brands. Growing global ambitions of Chinese companies and proceeding modernisation in the public and private sectors (especially among the vast pool of SMEs) will fuel investment in software in 2015. BMI expects software sales to grow 7.9%, to CNY 108.0 billion (EUR 16.2 billion).

IT services is the outperforming segment in China’s ICT market. As a result of increasing demand from both government and enterprise segments, underpinned by an expansion of network infrastructure and modernisation initiatives, BMI forecasts IT services to increase 16.1% in 2015, to CNY 242.6 billion (EUR 36.3 billion).

Our underwriting stance remains generally open for large ICT manufacturers and national/regional distributors, while we are more cautious with system integrators, retailers and online sellers, where competition is fierce and the financial situation of businesses often less strong. ICT is generally a low margin sector, and therefore businesses may invest into other fields to earn quick money, like microcredit companies, guarantee companies, and real estate. This may have worked well in the past, but has become more risky now due to tight liquidity in the market and downward pressure on real estate. Cross guarantee is widely used in bank lending to ICT traders, meaning that one company’s liquidity collapse could drag down others.

Related documents

1MB PDF