Atradius forecasts insolvencies across advanced markets to fall by 3.0% this year and 2.0% next year, particularly led by an increasingly robust recovery in the eurozone.

Summary

- Atradius presents its new insolvency forecasting model which offers a broader scope of macroeconomic developments to better predict insolvency developments.

- GDP growth across advanced markets is picking up in 2017 and 2018 supported by strengthening labour markets, higher confidence, and more supportive policies. Downside risks, especially policy uncertainty, have eased but are still concerns.

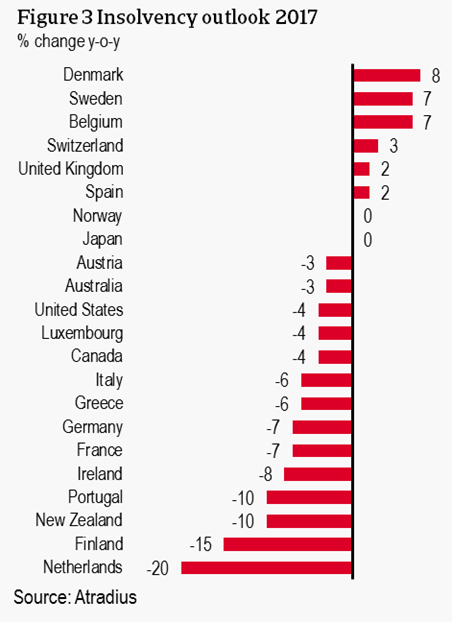

- Global business insolvencies are expected to decrease 3.0% this year and 2.0% next year, particularly led by an increasingly robust recovery in the eurozone.

Risks to the insolvency outlook remain tilted to the downside. Disorderly monetary tightening, equity market corrections, and a pronounced slowdown in China decreasing global import demand could all drive upward revisions, especially in 2018. Political uncertainty is also a persistent risk, with Brexit negotiations taking place as well as renegotiations of trade deals in the US.

New Atradius insolvency forecasting model

The Atradius Economic Research team has developed a new model to better predict corporate insolvencies in advanced markets. The foundation of the model is still the same: general business cycle indicators, such as GDP growth, are inversely related to insolvency growth. The predictive power is now improved by incorporating additional significant macroeconomic variables:

- The unemployment rate (or changes therein) is an input for health of the labour market

- Industrial production growth is a significant forward-looking indicator for business activity and economic performance

As before, this model is two-fold. On top of the quantitative model, expert judgment is applied. Deviations from the model outcome may be recommended by country experts based on other macroeconomic or financial developments, credit conditions, and historical insolvency trends. For further information, a more in-depth, non-technical model description will be released shortly.

Eurozone driving the brighter outlook

Economic momentum in the eurozone has been gathering pace since late 2016 and a broad-based recovery is finally underway. Domestic demand is picking up, supported by still-low inflation and ultra-loose monetary policy. Credit standards continue to ease across all loan categories and bank lending growth is accelerating, according to the ECB’s latest Bank Lending Survey. Exports are boosting GDP growth, supported by a stronger global economy and a weaker euro. Political risk has also eased following the loss of momentum for Eurosceptic parties in elections in Austria, France, and the Netherlands this year. Eurozone-wide, insolvencies are expected to decrease 6.0% this year, followed by -5.0% next year. Regional insolvencies remain 50% higher than in 2007.

The decline in insolvencies will again be led by the Netherlands (-20.0%). Despite the volume of bankruptcies already being historically low in the Netherlands, the total number of insolvencies in H1 was 23% lower than H1 of 2016. A continuation of this trend is expected, in line with robust, broad-based economic growth and post-crisis highs in consumer and producer confidence. We predict an easing in the pace in 2018 of decline as the annual volume is 60% of its 2007 level. Finland (-15%) is predicted to see the second-largest decline in insolvencies in 2017 before easing to a more stable 2% decline in 2018. Germany’s 2017-2018 outlook is also characteristically strong supported by exports, increasing domestic demand and government spending. Sentiment indicators have reached all-time highs, led by the manufacturing and construction sectors. This is expected to support a 7.0% decrease in 2017 and a 4.0% decline in 2018.

France, boosted by pro-growth policies under its new president, is forecast to see GDP expand 1.5% this year and 1.6% in 2018. After a strong 7.6% decline in insolvencies in 2016, we have revised the French 2017 outlook to a 7.0% decline. A further 6.0% decline in the total number of insolvencies in 2018 will bring the country’s annual count close to pre-crisis levels.

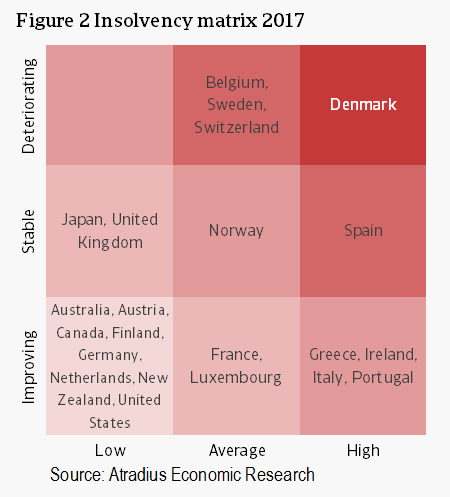

The recovery is also taking a strong hold, at last, in other economies, as shown by the prevalence of peripheral eurozone countries in the bottom right corner of the insolvency matrix in Figure 2 – showing high levels relative to 2007 but a downward trend forecast for 2017. Greece’s economy grew 0.4% q-o-q in Q1 of 2017 and full year growth is forecast at 1.1%, driven by private and government consumption. Manufacturing activity is also finally picking up. Corporate failures in Greece are forecast to finally tick down by 6.0% after nearly a decade of annual increases. We predict insolvencies will decline another 8.0% in 2018 but that the absolute level will remain three times that of 2007. The level of insolvencies in Portugal is also around three times higher than in 2007, but solid decreases of 10.0% and 6.0% this year and next could bring it down to about 270% of pre-crisis levels. GDP growth in Portugal is the fastest it has been in a decade. Ireland (-8.0%) is also enjoying steady declines in insolvencies already this year and we predict this to continue, bringing the level of insolvencies back toward normal levels. It is still twice as many annual bankruptcies than 2007 and the pace of decline is easing in line with GDP growth.

Spain is enjoying the highest rate of GDP growth in the eurozone thus far this year, marking its fourth year of expansion and steady job creation. From 2014 to 2016, Spain saw double digit declines in the annual number of bankruptcies. In this light, we previously forecast another 8.0% decline in Spain. However, H1 data has not come in as expected, showing a 4.0% increase compared to H1 of 2016. This could be driven by an increasing number of active companies (+5.2% in Q2 of 2017 compared to the year before) and/or on-going deleveraging in the private sector. There is little evidence though that this trend will continue. The economic expansion is broad-based and the outlook is positive. The labour market is also tightening with unemployment at an eight-year low of 17.2% of the active population. Thus we forecast the full-year change in insolvencies to be a more stable 2.0% increase before a 7.0% decline in 2018. Spain’s annual number of insolvencies is still five times its 2007 levels, the highest in the surveyed countries.

US continues strong performance but policy uncertainty remains downside risk

Across the Atlantic, the US economic outlook is also robust, which is reflected in high business confidence. One such measure is the Business Roundtable CEO Economic Outlook Index which looks at the plans of CEOs of the 200 largest US companies for spending, investment and sale projections over the coming six months. This index is well above its historical average and shows that the business environment is still very optimistic, especially for tax reforms. US GDP is expected to expand a solid 2.0% in 2017 and 2018. This forecast is however slightly more moderate due to a less expansionary fiscal policy than previously expected. The positive outlook is supported by strong jobs growth, very low and declining unemployment, and even firming wage pressure. In this environment, the number of bankruptcy filings is at historical lows. In Q3 of 2016, the number of bankruptcies in the US reached its lowest quarterly level since Q4 of 2006. We forecast a 4.0% decline in the overall number of insolvencies this year and a mild 2.0% decline in 2018, but uncertainty continues to weigh on the US outlook.

Following a trough in Q3 of last year, the number has been steadily climbing each quarter. This trend could continue and even worsen largely due to uncertainty which may reduce business investment. While policy uncertainty has receded since November, there remain risks to the insolvency outlook. NAFTA renegotiations for example could have severe implications for the US business outlook through lower investment in case of heightened uncertainty or business impediments. With strong economic and labour market data continuing to come in, a faster-than-expected monetary tightening path may also strain businesses’ balance sheets.

UK forecast to see an increase in insolvencies as growth slows and Brexit-negotiation uncertainty rises

Despite economic resilience over 2016 and high business confidence, insolvencies in the UK are on an upward trend. For the first time since 2011, total corporate failures increased last year, albeit by only 1.0%. With 7,567 underlying business liquidations in H1 of 2017, insolvencies are 1.7% higher than in the same period in 2016. This trend is expected to continue through this year and next as GDP growth eases. Higher inflation is increasingly feeding into lower real earnings, weighing on private consumption, the main driver of UK economic activity. This is likely to be exacerbated by expected tightening in consumer credit by banks. The most vulnerable sectors are consumer-oriented like retail trade and accommodation & food services.

The manufacturing sector on the other hand, which accounts for about 15% of the UK’s economy, is supported by the weak sterling which boosts export competitiveness. This has contributed to the resilience of the UK economy thus far and manufacturing surveys show confidence at record highs. Annual industrial production growth is still positive, driven by increased mining activity. Manufacturing production, however, has been flat or falling for the first six months of the year though, led by the transport sector. This could put further upward pressure on insolvencies. We expect GDP growth to ease to 1.6% in 2017 and annual insolvencies to increase 2.0%. With Brexit negotiations with the EU underway, uncertainty is rising and is projected to weigh on business investment, bringing GDP growth to only 1.0% in 2018. We predict corporate failures to increase by a further 4.0% next year.