Depreciation of the Euro against the British Pound has made UK products and services less attractive to eurozone buyers.

Summary

- Strong economic performance in the UK has caused the pound to appreciate. This trend has intensified this year due to weak growth and expansionary monetary policy in the Eurozone.

- British exports may lose competitiveness in the Eurozone, dragging on economic growth in the UK. Importers will benefit from less expensive Eurozone imports. Households in the UK should benefit from higher spending power.

- To rebalance the economy toward export-led growth, the UK should diversify its export destinations. Exports continue to primarily go to the Eurozone, but the rate of growth of exports to emerging markets outpaces that to the Eurozone.

Falling euro puts additional pressure on pound

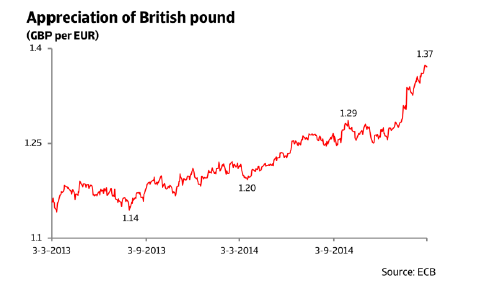

The UK economy grew by 2.6% in 2014, the highest rate in the G-7, as the number of unemployed fell by over 20% with 5.7% of the population unemployed in December 2014, the lowest rate since mid-2008. A side effect of the UK’s strong economic performance has been a steady rise in the pound since early 2013. The value of the pound has gradually increased by 20.4% relative to the euro since March 2013 including a sharp drop of 7% since the beginning of 2015 alone. The pound closed at EUR 1.37 on 2 March 2015, the highest level seen since 2007.

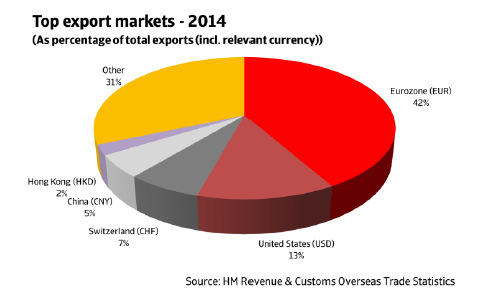

The latest increases in the pound’s value have been exacerbated by the euro’s performance. The Eurozone is by far the UK’s largest export market, accounting for 42% of exports in 2014. Therefore, the pound sterling is inherently sensitive to the euro’s movements.

Over the past year, the euro has been losing value, most sharply over the past three months. The currency’s depreciation is primarily motivated by weak economic growth in the Eurozone and the response by the European Central Bank (ECB). In order to strengthen the Eurozone recovery, the ECB has taken exceedingly aggressive measures to boost spending and inflation. Long-term interest rates have been driven down to just 0.05%, making euro-denominated bonds less attractive, encouraging domestic spending and sending investors to seek higher yields outside the Eurozone, depreciating the euro. The larger-than-expected quantitative easing package – amounting to EUR 60 billion of asset purchases per month until September 2016 – announced in late January has further driven down government bond yields and devalued the euro.

The euro’s depreciation is perceived as a welcome effect to the ECB as it may provide an extra boost to inflation and to overall economic growth in the Eurozone. But the devaluation of a currency implies the appreciation of another – one such currency being Great Britain’s pound.

In July 2014 already, the IMF warned that the pound was overvalued and causing a reduction in major UK companies’ profits by more than GBP 1 billion as well as preventing the rebalancing of the economy. Robust growth has been putting upward pressure on the pound as well as market expectations that the Bank of England (BoE) may raise rates in 2016. The depreciation of the euro is asserting further pressure.

Exporters lose, importers win

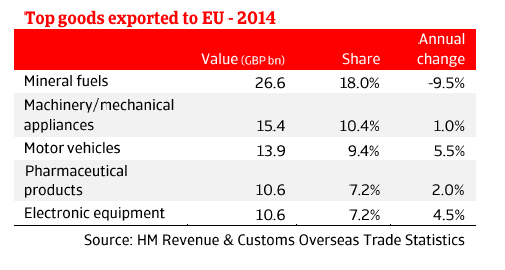

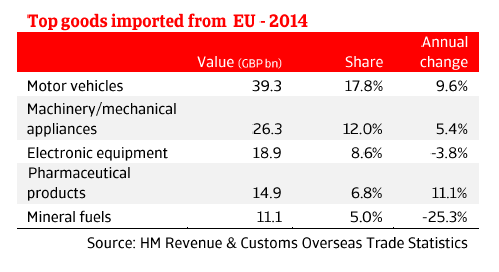

In order to sustain robust economic growth, the UK government is aiming to rebalance the economy away from consumer spending and towards higher productivity and more exports. There remains significant progress to be made on this front, as the UK remains a net importer with imports exceeding exports by GBP 6.3 billion in December 2014. but difficult conditions in the Eurozone, the UK’s most important trade partner, have contributed to the widening of the trade deficit to GBP 34.8 billion in 2014. Businesses that depend on exporting their products are adversely affected by the low euro as exports to the Eurozone will be relatively more expensive, either reducing demand for UK exports or forcing British firms to reduce their profit margins. A second hit to exporters may come in the form of a “translation effect.” Revenue coming from overseas may translate poorly back into earnings reports denoted in sterling.

The price of importing European goods however decreases thanks to the weaker euro, benefiting British companies that depend on imports from the Eurozone. Switching from domestic supplies to imports, particularly from the Eurozone, of interchangeable products could offer an opportunity for companies to lower the costs of production. At the same time, however, this could further harm domestic manufacturers.

The risks of an appreciating pound and depreciating euro also extend beyond trade with the Eurozone. For instance, Switzerland, accounting for 7% of the UK’s exports (third largest market when considering the Eurozone as a single market), as well as Sweden, have adjusted their monetary policy in order to mitigate the impact of the falling euro. Thus, these countries’ currencies have also lost value against the pound, indicating similar risks for UK exporters to these markets.

Many countries peg their currencies to the euro as a safety measure against exchange rate fluctuations that may reduce profits and discourage trade. These include Bulgaria and Denmark as well as many central and west African countries. British companies that engage in trade in these markets also face the same issues for exports and benefits for imports.

British households stand to gain from the weaker euro. Consumer spending power should rise as products originating from the Eurozone lose value in pounds. This, combined with depressed oil prices, should increase imports and put further strain on the trade balance. Both of these factors also contribute to the low inflation rate which fell from 0.5% in December 2014 to 0.3% in January 2015, the lowest rate recorded since the UK government began recording the comparable CPI measure in 1997. This should benefit households as the rate of growth in wages will finally outpace the rate of inflation. On the other hand however, this may further damage domestic businesses as consumers opt for foreign-made goods.

New markets

The BoE predicts the economy will expand by 2.9% in 2015 – its fastest rate in nearly a decade. Concerns are rising however regarding the low inflation rates, with the BoE Governor raising the possibility of an even further rate cut should inflation remain weak for a prolonged period. But current trends show lower oil prices as well as low inflation and higher wage growth are helping to fuel robust growth through putting more money in the pockets of consumers and businesses. This will put upward pressure on the pound which may be intensified by an expected rate hike by BoE in early 2016.

At the same time, growth in the Eurozone is forecast to remain tepid this year and the ECB has committed itself to continue quantitative easing until at least late 2016. This suggests the euro is likely to fall further as well. Therefore, British exporters may do better by looking to other, fast-growing emerging markets, in order to pave a sustainable, rebalanced, export-led recovery.

The share of total exports to the Eurozone has fallen from 51.2% in 2007 to 41.7% in 2014 while exports to Brazil, Russia, India, China, and South Africa (BRICS) have increased from 5.7% to 9.2% of the total share in the same period.

Of the UK’s top 10 export destinations (considering Eurozone countries as individual markets), China is the only emerging market and export prospects there are waning as Chinese growth is expected to continue cooling. Besides the United States, all other top export markets are in Western Europe. Strong growth in the United States and the relative stability of the exchange rate between the GBP and USD indicate that the UK’s second largest trading partner remains a promising destination for UK exports. But UK businesses will have to compete against the more competitive prices from Eurozone exporters.

Increasing trade to new markets offers a natural hedge for British firms, as it diversifies some currency risks and follows demand. The strength of demand for exports is the most important thing for British firms, even more so than the exchange rate, so increasing trade with more buoyant economies is a key strategy.

“Whilst there are plenty of positives to focus upon when we look at the performance of the UK economy, there is no doubt that the lack of growth in export activity has been a real disappointment,” says Simon Rockett, Senior Manager of UK Underwriting at Atradius. “The Eurozone continues to be our main trading partner, and through a combination of a lack of demand and the strength of Sterling the opportunities for UK exporters in traditional markets are unlikely to increase. Businesses throughout the UK really need to look outside of the Eurozone for growth and this is where Atradius can really add value. With a presence through 160 offices in 50 countries we have Risk Underwriting teams who have the experience and information to assist UK exporters operating in any industry to succeed.”

Related documents

1012KB PDF