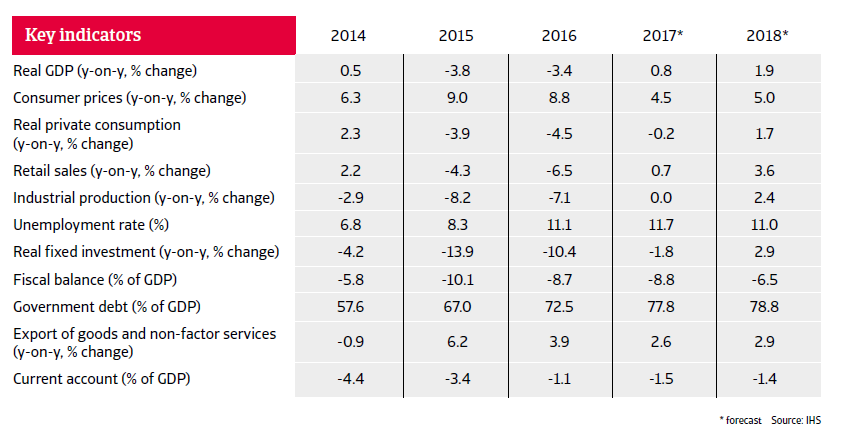

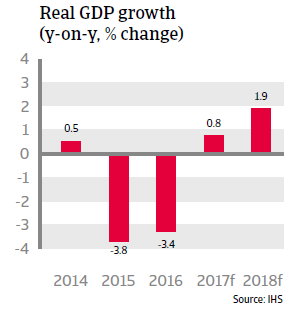

While in 2017 a modest economic rebound after two years of contraction is expected, Brazilian business insolvencies will continue to increase by about 10%.

Political situation

Head of state/government:

President Michel Temer (since August 2016)

Population:

206.1 million (est.)

High political uncertainty remains

At the end of August 2016 the Brazilian Senate voted to impeach President Dilma Rousseff of the leftist Partido dos Trabalhadores (PT), finding her guilty of breaking budgetary laws, and confirmed Michel Temer of the centrist Partido do Movimento Democrático Brasileiro (PMDB) as president until the end of 2018. Although Mr Temer has a majority in Congress, governability will continue to be hindered by the on-going corruption investigations at the state oil company Petrobras. State prosecutors alleged leading construction companies and other businesses paid huge bribes to high-ranking officials of Petrobras and to politicians in return for contracts. So far, over half of Congress members and even President Temer have been implicated, which potentially could lead to his resignation should the bribery allegations materialise.

Economic situation

Economic reforms tackled by the new government

Since taking office, President Temer and his economic advisors launched more orthodox economic policies in order to improve government finances, increase investors sentiment and pull the economy out of crisis. This includes constitutional amendments to curb public spending growth and to improve the credibility of the Central Bank. The administration also started to tackle much needed pension and social security system reforms, to address labour market rigidity and reduce bureaucracy, but progress in those areas is expected to be very slow in the current volatile political environment.

A modest rebound after two years of contraction expected

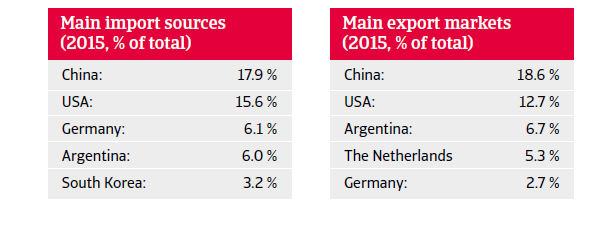

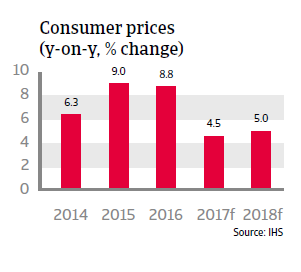

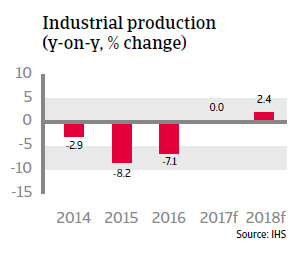

However, the economic environment will remain challenging, given a much needed fiscal policy adjustment, high unemployment of more than 10%, a weak manufacturing sector and recent declines in business and consumer confidence. Exports have so far contributed positively to economic growth, but orders indicate a lower increase in 2017. Currency volatility is likely to persist, given the current political volatility and uncertainty over US trade policies, which could lead to another depreciation.

Due to the economic contraction, business insolvencies have increased significantly (in particular judicial recovery cases rose about 45% year-on-year in 2016), and this trend is expected to continue as the rebound is feeble and banks are still reluctant to lend. Business insolvencies are expected to increase further in 2017, by about 10%.

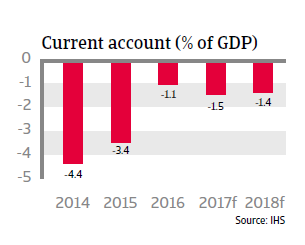

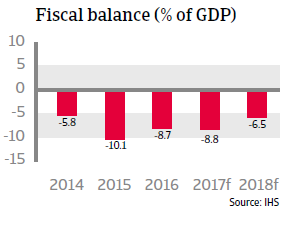

Government debt to increase above 75% of GDP in 2017

Currency, refinancing and sovereign default risks are mitigated by the fact that 85% of government debt is financed domestically (95% in local currency) at an average maturity of almost seven years, while the government is a net-external creditor. However, government debt has increased to 72.5% of GDP in 2016 and is forecast to rise above 90% in 2020 before levelling off; which is faster and higher than previously expected. Therefore, progress in containing government debt is crucial in retaining business and investors’ confidence and the country´s creditworthiness.

Corporate foreign debt has increased sharply, but remains manageable for now

Brazil´s banking sector is well regulated and sufficiently capitalised. The system is not dollarized and the dependency on external wholesale financing is low, shielding the banking system from adverse shocks. That said, the share of non-performing loans has increased to almost 4% in 2016, with mainly small- and medium-sized businesses affected.

Still vulnerable to changing investors’ sentiment, but resistant to major shocks